2025 Silver Nanowire Transparent Electrode Manufacturing Market Report: Trends, Forecasts, and Strategic Insights for the Next 5 Years

- Executive Summary and Market Overview

- Key Technology Trends in Silver Nanowire Transparent Electrodes

- Competitive Landscape and Leading Manufacturers

- Market Growth Forecasts (2025–2030): CAGR, Volume, and Revenue Projections

- Regional Analysis: North America, Europe, Asia-Pacific, and Rest of World

- Future Outlook: Emerging Applications and Innovation Pathways

- Challenges, Risks, and Strategic Opportunities for Stakeholders

- Sources & References

Executive Summary and Market Overview

The global market for silver nanowire transparent electrode manufacturing is poised for significant growth in 2025, driven by escalating demand for flexible, lightweight, and highly conductive materials in next-generation electronic devices. Silver nanowire (AgNW) transparent electrodes are rapidly emerging as a preferred alternative to traditional indium tin oxide (ITO) due to their superior flexibility, lower processing temperatures, and cost-effectiveness, especially in applications such as touchscreens, OLED displays, solar cells, and wearable electronics.

According to recent industry analyses, the silver nanowire transparent electrode market is expected to achieve a compound annual growth rate (CAGR) exceeding 20% through 2025, with the Asia-Pacific region leading both production and consumption. This growth is underpinned by robust investments in consumer electronics manufacturing, particularly in China, South Korea, and Japan, where companies are aggressively pursuing advanced display technologies and flexible device architectures (MarketsandMarkets).

Key market drivers include the increasing adoption of flexible and foldable displays, the proliferation of smart wearable devices, and the ongoing transition toward more sustainable and energy-efficient photovoltaic solutions. Silver nanowire electrodes offer high optical transparency and electrical conductivity, making them ideal for these applications. Furthermore, the global shortage and price volatility of indium have accelerated the shift toward silver nanowire-based alternatives (IDTechEx).

Major industry players such as Cambrios, C3Nano, and NanoPyxis are investing heavily in scaling up production capacities and refining manufacturing processes to enhance product performance and reduce costs. Strategic collaborations between material suppliers, device manufacturers, and research institutions are further accelerating innovation and commercialization.

Despite the promising outlook, the market faces challenges related to large-scale manufacturing consistency, long-term stability of silver nanowire networks, and integration with existing device fabrication processes. However, ongoing advancements in synthesis techniques, coating technologies, and encapsulation methods are expected to address these hurdles, paving the way for broader adoption across multiple high-growth sectors.

In summary, 2025 is set to be a pivotal year for silver nanowire transparent electrode manufacturing, with strong market momentum, technological innovation, and expanding end-use applications positioning the sector for robust expansion and increased competitiveness in the global transparent conductor landscape.

Key Technology Trends in Silver Nanowire Transparent Electrodes

Silver nanowire (AgNW) transparent electrode manufacturing is undergoing rapid technological evolution, driven by the demand for flexible, lightweight, and highly conductive alternatives to traditional indium tin oxide (ITO) electrodes. In 2025, several key technology trends are shaping the production landscape, focusing on scalability, cost reduction, and performance enhancement.

One of the most significant advancements is the refinement of solution-based coating techniques, such as slot-die coating, spray coating, and roll-to-roll (R2R) processing. These methods enable large-area, uniform deposition of AgNWs on flexible substrates, supporting high-throughput manufacturing essential for commercial applications in touch panels, OLED displays, and photovoltaics. Companies like Cambrios and NovaCentrix are at the forefront, leveraging R2R processes to scale up production while maintaining electrode performance.

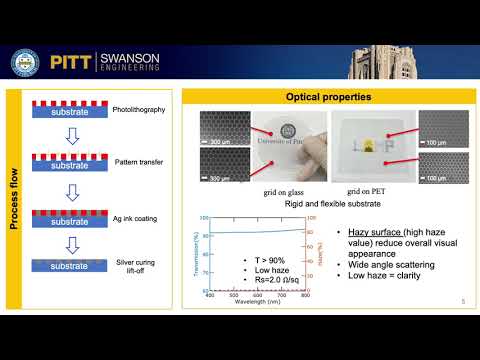

Another trend is the integration of hybrid structures, where AgNWs are combined with materials such as graphene, conductive polymers, or metal meshes. This approach addresses challenges like surface roughness, junction resistance, and mechanical durability. For instance, hybrid electrodes can achieve sheet resistances below 10 Ω/sq with over 90% optical transmittance, rivaling or surpassing ITO benchmarks, as reported by IDTechEx.

- Post-treatment innovations: Techniques such as photonic sintering, plasma treatment, and chemical welding are being adopted to improve nanowire connectivity and reduce contact resistance without damaging flexible substrates. These methods enhance conductivity and mechanical stability, crucial for foldable and wearable electronics.

- Material purity and nanowire morphology: Advances in synthesis allow for precise control over nanowire length, diameter, and aspect ratio, directly impacting film conductivity and transparency. High-purity, long-aspect-ratio nanowires are now commercially available, enabling lower percolation thresholds and improved film uniformity.

- Environmental and cost considerations: Manufacturers are increasingly focusing on green chemistry approaches and recycling of silver from production waste, responding to both regulatory pressures and the high cost of silver. This trend is supported by research from organizations like Fraunhofer, which explores sustainable manufacturing pathways.

In summary, the 2025 landscape for silver nanowire transparent electrode manufacturing is defined by scalable deposition technologies, hybrid material integration, advanced post-processing, and sustainability initiatives. These trends are collectively driving the adoption of AgNW electrodes in next-generation optoelectronic devices.

Competitive Landscape and Leading Manufacturers

The competitive landscape of the silver nanowire transparent electrode manufacturing market in 2025 is characterized by a mix of established material science companies, innovative startups, and regional players, all vying for market share in applications such as touch panels, OLED lighting, flexible displays, and photovoltaics. The market is driven by the demand for flexible, highly conductive, and transparent alternatives to traditional indium tin oxide (ITO) electrodes, with silver nanowires offering superior mechanical flexibility and lower processing costs.

Leading manufacturers in this sector include Cambrios, widely recognized for its pioneering work in silver nanowire inks and coatings, and C3Nano, which has developed proprietary nanowire synthesis and coating technologies to enhance conductivity and transparency. Sekisui Chemical and TDK Corporation are also prominent, leveraging their expertise in advanced materials and large-scale manufacturing to supply high-quality silver nanowire films for consumer electronics and automotive applications.

Asian manufacturers, particularly in China and South Korea, have rapidly scaled up production capacities, benefiting from strong domestic demand and government support for next-generation display technologies. Companies such as Blue Nano and Nanosys are notable for their integration of silver nanowire electrodes into commercial products, including touch sensors and flexible displays. These firms often collaborate with display panel manufacturers to optimize electrode performance and cost efficiency.

The competitive environment is further shaped by ongoing R&D investments aimed at improving nanowire uniformity, adhesion, and long-term stability, as well as reducing haze and production costs. Intellectual property remains a key differentiator, with leading players holding extensive patent portfolios covering synthesis methods, ink formulations, and coating processes. Strategic partnerships and licensing agreements are common, enabling technology transfer and accelerating commercialization.

Overall, the silver nanowire transparent electrode market in 2025 is marked by intense competition, rapid technological advancements, and a growing emphasis on scalability and integration into mass-market electronics. The ability to deliver high-performance, cost-effective solutions will determine the long-term leadership positions in this dynamic sector.

Market Growth Forecasts (2025–2030): CAGR, Volume, and Revenue Projections

The global market for silver nanowire transparent electrode manufacturing is poised for robust growth between 2025 and 2030, driven by expanding applications in touchscreens, flexible displays, photovoltaics, and emerging wearable electronics. According to projections from MarketsandMarkets, the silver nanowire market—including its use in transparent electrodes—is expected to register a compound annual growth rate (CAGR) of approximately 25% during this period. This surge is attributed to the material’s superior conductivity, flexibility, and transparency compared to traditional indium tin oxide (ITO) electrodes.

In terms of volume, the demand for silver nanowires is forecast to reach over 1,200 metric tons by 2030, up from an estimated 400 metric tons in 2025. This significant increase is underpinned by the rapid adoption of silver nanowire-based electrodes in next-generation consumer electronics and the scaling up of manufacturing capacities by key industry players such as Cambrios and Blue Nano.

Revenue projections for the silver nanowire transparent electrode manufacturing sector are equally optimistic. The market is anticipated to grow from a valuation of approximately USD 350 million in 2025 to surpass USD 1.1 billion by 2030, as reported by IDTechEx. This growth is fueled by increasing investments in R&D, the commercialization of flexible and foldable devices, and the ongoing shift toward sustainable and cost-effective alternatives to ITO.

- CAGR (2025–2030): ~25%

- Volume (2030): >1,200 metric tons

- Revenue (2030): >USD 1.1 billion

Regionally, Asia-Pacific is expected to dominate both production and consumption, led by countries such as China, South Korea, and Japan, where electronics manufacturing ecosystems are highly developed. North America and Europe are also projected to witness substantial growth, particularly in the context of advanced display technologies and renewable energy applications. Overall, the silver nanowire transparent electrode manufacturing market is set for dynamic expansion, with technological advancements and end-user demand shaping its trajectory through 2030.

Regional Analysis: North America, Europe, Asia-Pacific, and Rest of World

The regional landscape for silver nanowire transparent electrode manufacturing in 2025 is shaped by varying levels of technological advancement, investment, and end-user demand across North America, Europe, Asia-Pacific, and the Rest of the World (RoW).

North America remains a significant hub, driven by robust R&D activities and the presence of leading electronics and display manufacturers. The United States, in particular, benefits from strong collaborations between academic institutions and industry players, fostering innovation in nanomaterials and scalable production techniques. The region’s focus on flexible electronics and next-generation touch panels continues to spur demand for high-performance transparent electrodes. Additionally, government funding and initiatives supporting advanced materials research further bolster the market’s growth trajectory in North America (National Science Foundation).

Europe is characterized by stringent environmental regulations and a strong emphasis on sustainable manufacturing. European manufacturers are increasingly adopting silver nanowire-based electrodes as alternatives to indium tin oxide (ITO), aligning with the region’s push for eco-friendly and resource-efficient solutions. Germany, the UK, and France are at the forefront, leveraging their established electronics and automotive sectors to integrate these materials into displays, photovoltaics, and smart windows. The European Union’s funding for nanotechnology research and its focus on circular economy principles are expected to accelerate adoption rates (European Commission).

- Asia-Pacific dominates global production and consumption, led by China, South Korea, and Japan. The region’s competitive advantage stems from large-scale manufacturing capabilities, cost-effective labor, and a dense network of electronics OEMs. China, in particular, is investing heavily in nanomaterial production to support its rapidly expanding display and solar industries. South Korea and Japan continue to innovate in flexible and wearable electronics, driving further demand for silver nanowire transparent electrodes. Strategic partnerships between local manufacturers and global technology firms are also accelerating commercialization (Statista).

- Rest of World (RoW) includes emerging markets in Latin America, the Middle East, and Africa. While adoption is currently limited by infrastructure and investment constraints, these regions are expected to witness gradual growth as global supply chains expand and the cost of silver nanowire technology decreases. Initiatives to localize electronics manufacturing and renewable energy projects may further stimulate demand in the medium term (International Data Corporation (IDC)).

Future Outlook: Emerging Applications and Innovation Pathways

The future outlook for silver nanowire (AgNW) transparent electrode manufacturing in 2025 is shaped by a convergence of technological innovation, expanding application domains, and evolving market demands. As the limitations of traditional indium tin oxide (ITO) electrodes become more pronounced—particularly in terms of flexibility, cost, and supply chain volatility—AgNW-based transparent electrodes are poised to capture a larger share of the market for next-generation optoelectronic devices.

Emerging applications are a key driver of this shift. In 2025, the proliferation of flexible and wearable electronics, such as foldable smartphones, rollable displays, and smart textiles, is expected to accelerate the adoption of AgNW electrodes due to their superior mechanical flexibility and conductivity. The automotive sector is also exploring AgNW films for use in curved touch panels and heads-up displays, leveraging their ability to maintain transparency and performance under deformation. Additionally, the rapid growth of the Internet of Things (IoT) ecosystem is fueling demand for transparent, flexible sensors and antennas, where AgNW networks offer a compelling solution IDTechEx.

Innovation pathways in manufacturing are focused on scalability, cost reduction, and performance enhancement. Roll-to-roll (R2R) processing and inkjet printing are gaining traction as scalable methods for depositing AgNW networks onto large-area substrates, enabling high-throughput production suitable for commercial applications. Advances in nanowire synthesis—such as improved control over aspect ratio and surface chemistry—are enhancing film uniformity, optical clarity, and electrical conductivity. Hybrid electrode structures, which combine AgNWs with materials like graphene or conductive polymers, are being developed to further improve durability, reduce haze, and mitigate issues such as junction resistance and oxidation Frost & Sullivan.

- Increased investment in R&D is expected from both established electronics manufacturers and startups, aiming to optimize AgNW formulations for specific end-use cases.

- Strategic partnerships between material suppliers and device makers are likely to accelerate commercialization and integration into mainstream products.

- Regulatory and sustainability considerations are prompting research into greener synthesis methods and recycling of AgNW-based films.

Overall, the outlook for silver nanowire transparent electrode manufacturing in 2025 is robust, with innovation and application diversification driving market expansion and technological maturation MarketsandMarkets.

Challenges, Risks, and Strategic Opportunities for Stakeholders

The manufacturing of silver nanowire (AgNW) transparent electrodes in 2025 presents a complex landscape of challenges, risks, and strategic opportunities for stakeholders across the value chain. As demand for flexible displays, touchscreens, and next-generation photovoltaics accelerates, manufacturers must navigate technical, economic, and regulatory hurdles while capitalizing on emerging market trends.

Challenges and Risks:

- Material Costs and Supply Chain Volatility: Silver remains a costly raw material, and price fluctuations can significantly impact production economics. Geopolitical tensions and supply chain disruptions, as seen in recent years, further exacerbate procurement risks for high-purity silver required in nanowire synthesis (The Silver Institute).

- Scalability and Uniformity: Achieving consistent nanowire morphology and uniform electrode coatings at industrial scale remains a technical bottleneck. Variations in nanowire length, diameter, and dispersion can lead to performance inconsistencies, affecting device yield and reliability (IDTechEx).

- Competition from Alternative Materials: Indium tin oxide (ITO) continues to dominate the transparent electrode market, while emerging materials such as graphene and conductive polymers are gaining traction. This intensifies the need for AgNW manufacturers to demonstrate clear performance and cost advantages (MarketsandMarkets).

- Environmental and Regulatory Pressures: The use of silver and certain solvents in nanowire production raises environmental and occupational health concerns. Stricter regulations on waste management and chemical usage may increase compliance costs and necessitate process innovation (U.S. Environmental Protection Agency).

Strategic Opportunities:

- Process Innovation: Stakeholders investing in greener synthesis methods, such as water-based or solvent-free processes, can reduce environmental impact and regulatory risk, while potentially lowering costs (Fraunhofer Society).

- Product Differentiation: Developing AgNW electrodes with enhanced flexibility, stretchability, or compatibility with roll-to-roll manufacturing can open new applications in wearables, automotive displays, and smart windows (FlexTech Alliance).

- Strategic Partnerships: Collaborations with device manufacturers and material suppliers can accelerate technology validation, secure supply chains, and facilitate market entry for next-generation products.

- Market Diversification: Expanding into niche markets such as biomedical sensors or transparent heaters can mitigate risks associated with mainstream display and photovoltaic sectors.

Sources & References

- MarketsandMarkets

- IDTechEx

- NovaCentrix

- Fraunhofer

- Sekisui Chemical

- National Science Foundation

- European Commission

- Statista

- International Data Corporation (IDC)

- Frost & Sullivan

- The Silver Institute